What Legal Documents Do You Need to Raise a Fund?

Once you’ve decided on the structure and terms of your fund or syndication, you need to formalize your offering. In this chapter, we’ll discuss the key legal documents you need to raise an investment fund or syndication. We’ll divide the documents into two main categories:

- Principal Fund Documents: These are the main, large documents investors will review.

- Ancillary Fund Documents: These are internal documents, which are more boilerplate and less exciting.

PRINCIPAL FUND DOCUMENTS

First, let’s hit the big-ticket items. These are the substantive documents LPs will review (and in some cases sign) before investing.

1. Summary of Terms

Your summary of terms lists the high-level terms you chose in Chapter 6. Don’t be fooled though, it’s often quite detailed. A summary of terms might be five to ten pages for a simple syndication and ten to twenty pages for a multi-asset investment fund.

If you have a PPM (discussed below), your summary of terms will be in the PPM. If you don’t have a PPM, you’ll typically give your summary of terms to prospective LPs as a standalone document in your data room.

As discussed in Chapter 1, you might choose to circulate your summary of terms, along with your marketing deck, as your primary marketing materials before working with your lawyer to draft the remaining long-form legal documents discussed in this chapter.

Typically, nobody signs the summary of terms. It’s just an informational document.

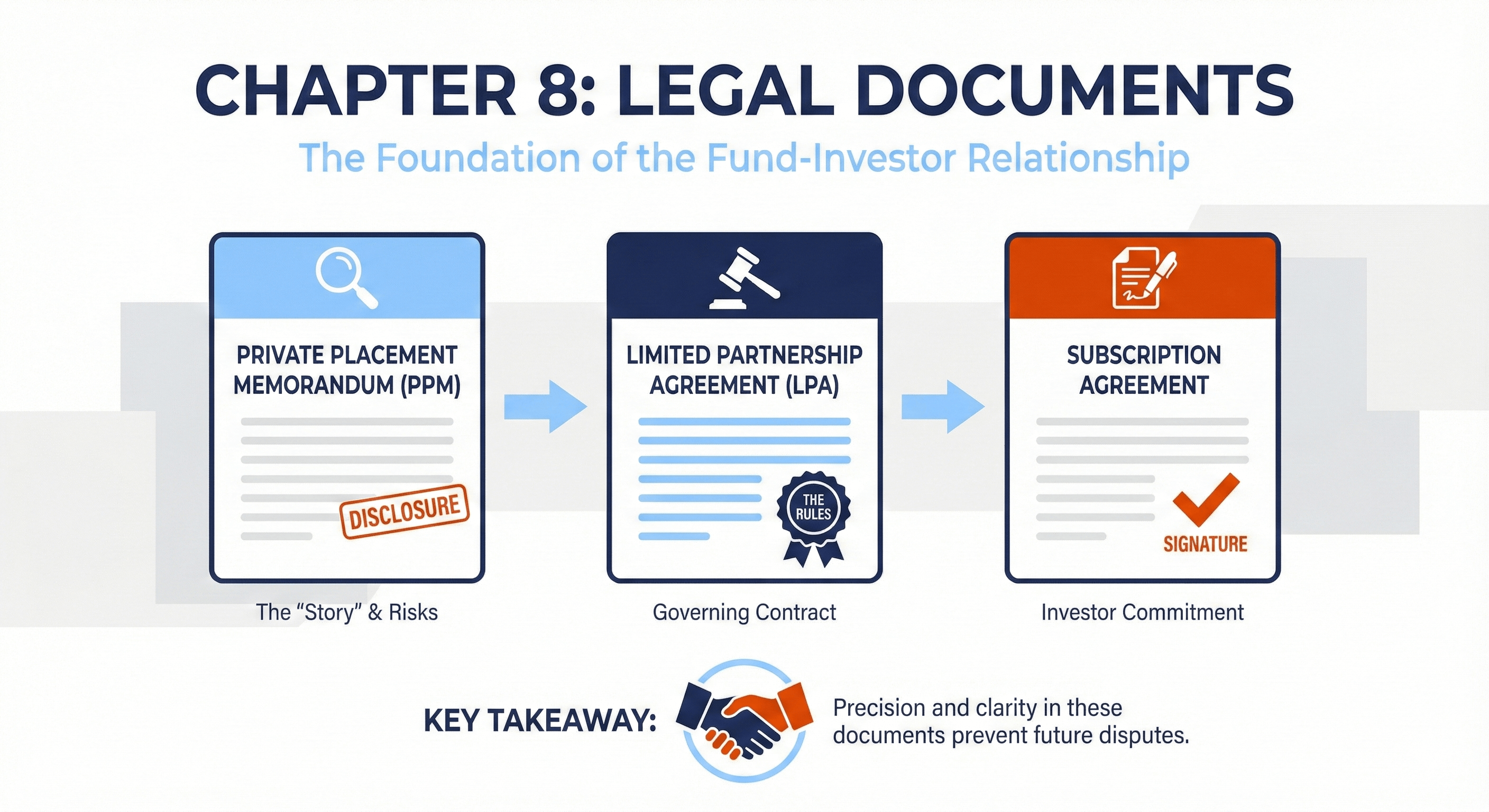

2. Limited Partnership Agreement (LPA)

The LPA is the main legal contract between the GP and the LPs. In a simple syndication, it might be thirty-five to forty pages long. A multi-asset fund might have an LPA of eighty to one hundred pages or more. The LPA is essentially the expanded, fancy, legalese version of your summary of terms.

In most cases, the LPA signed at your fund’s initial closing date will be the “Amended and Restated LPA.” Early in the fund-formation process, your lawyer will typically draft a very short “initial LPA” that will enable you to formally set up the fund entity (usually a limited partnership), open bank accounts, and otherwise prepare for the initial closing. At the initial closing, everyone will enter into the long-form Amended and Restated LPA.

Throughout this book, I refer to this document as the LPA. However, if your fund or syndication is an LLC (instead of a limited partnership), this agreement is technically called the LLC Agreement or the Operating Agreement (as LLCs don’t have LPAs). These are all synonyms for the same thing: the contract between the GP and the LPs.

In many funds, the GP signs the LPA both on their own behalf and on behalf of the LPs via a power of attorney granted in the subscription documents (discussed below). In other funds, all LPs sign the LPA (though this is uncommon in institutional-grade funds and syndications).

⚠ FUND TRAP #8: CUTTING CORNERS ON LEGAL DOCUMENTS

This is an admittedly self-serving statement, but you absolutely must work with experts to draft your fund or syndication documents. If you fail to do so, you might accidentally run afoul of laws and regulations. In addition, your legal documents may not reflect the deal you thought you were making with LPs. This happens more than you might think.

People often come to the firm where I work to have us “fix” their fund. In one instance, a fund manager (who had miraculously already raised two funds) had used a “general practitioner” to set up their first two investment funds, and they came to regret it. They thought they were going to fund part of their GP commitment with an acquisition fee waiver (see Chapter 16), but the required language was nowhere to be found in the legal documents. Also, the carried interest waterfall was switched, with the LPs getting 30 percent of the profits and the GP getting 70 percent. These mistakes can (usually) be fixed, but it involves amending the LPA with your tail between your legs (and admitting to LPs that you—or your lawyer—were careless).

The fund documents are the deal between the GP and the LPs. If you screw those up, the whole fund might be in jeopardy. Take this seriously!

3. Subscription Documents (Sub Docs)

The subscription documents are what LPs sign to officially invest in your fund or syndication. The sub docs usually have a few key sections:

- Representations and Warranties: The LPs agree to a long list of representations and warranties for the benefit of the GP and their affiliates.

- Investor Questionnaire: LPs answer questions about their backgrounds, wealth, and the vehicles through which they’re investing (if they’re not investing in their individual capacity). The questionnaire is necessary so the fund can comply with the laws and regulations we’ll discuss in Part II.

- Signature Pages: LPs indicate their investment amounts. In many funds, they also sign a power of attorney entitling the GP to sign the LPA on their behalf.

- Disclosure Statement: If the fund does not have a PPM, the subscription documents should contain all the required legal disclosures and risk factors. See the section on PPMs below.

4. Private Placement Memorandum (PPM)

The PPM is a big, fancy marketing document. It looks very official. It is, however, not strictly necessary.

The PPM has a split personality. The first half of the document is filled with flowery language, positive vibes, and delightful graphs describing how great the GP is. But then…there’s a sudden shift. The second half of the PPM is depressed, nervous, and timid. You learn that investing is risky, and there are 101 ways to lose your money.

Raising Money Without a PPM

Some smaller funds and syndications raise money without a PPM. The scary legal stuff is necessary, though. If you forego a PPM, you should put the legal disclosures and risk factors in the subscription agreement so investors can review them before deciding to invest. The positive marketing language can go into your marketing deck. As such, the deck becomes your sword, and the disclosures in the sub docs your shield.

In practice, many funds still choose to have a full PPM (especially larger funds and those relying on the 506(c) exemption under the Securities Act—discussed in Chapter 12).

Complex Fund Structures

If you have special regulatory or tax requirements that result in you needing to form a parallel fund, feeder fund, or other alternative investment vehicle, you will generally need a separate LPA and sub docs for each vehicle. In many cases, the PPMs can be combined. You’ll also need to set up separate legal entities (and potentially draft ancillary documents) for each parallel or feeder vehicle.

ANCILLARY FUND DOCUMENTS

In addition to the documents discussed above, you’ll likely need some or all of the following side documents:

- Marketing Deck: A slide deck outlining your thesis, track record, and fund terms. You should have your lawyer review this before sending it to prospective investors.

- Management Agreement: If you have both a GP and a ManCo, you’ll often have a short agreement that designates the ManCo as the fund’s management company in exchange for receiving the management fee.

- Entity Formation Documents: These include formation certificates, foreign qualifications, employer identification numbers, and initial governing agreements.

- Comprehensive GP/ManCo Documents: If you aren’t a sole GP, you likely want documents laying out the deal between you and the other fund principals, including what happens if someone dies, leaves the firm, or commits a bad act.

- Rule 506 "Covered Person" Questionnaire: If you’re using Regulation D, you may want documents confirming principals aren’t disqualified from using Regulation D.

- Closing Resolutions: A blanket consent document authorizing and ratifying everything the GP did to set up the fund and admit investors.

Obviously, this isn’t a comprehensive list—for that, work with your lawyer! We’ll talk through the mechanics of holding your initial closing and admitting LPs in Chapter 10.

At this point, you’ve collaborated with your lawyer to create impeccable documents you’re ready to send out to potential investors. But what if the investors want to negotiate the terms of the fund documents? We’ll cover negotiation strategies in the next chapter.

More Fundamentals Chapters

Let's Build Something Together

Please provide some background on yourself, your track record (if applicable), and your goals. We're excited to get started.