The Investment Advisers Act of 1940

In this chapter, we’re looking at the third major law that governs investment funds and syndications: the Investment Advisers Act of 1940. As the name suggests, this law applies to investment advisers — and many fund managers fall squarely into that category.

What Is an Investment Adviser?

The Investment Advisers Act defines an investment adviser as:

Any person who, for compensation, engages in the business of advising others — directly or through publications or writings — about the value of securities or the advisability of investing in, purchasing, or selling securities.

In simpler terms, you are considered an investment adviser if:

- You give advice about securities,

- You do so as a business, and

- You receive compensation for it.

Let’s unpack these components.

“Engages in the Business”

The SEC interprets this broadly. You may be considered “in the business” if you:

- Hold yourself out as an investment adviser or financial professional

- Provide advice regularly

- Charge any fee for investment advice

You do not need to be giving daily stock picks to qualify — even periodic advice counts.

“Advising Others…as to the Value of Securities”

This includes recommendations about:

- Stocks, bonds, mutual funds, or LP interests

- Market trends or asset allocation

- Manager selection

- Market valuations or reports involving securities

Most private fund managers fall under this definition because their core activity involves evaluating and acquiring securities.

Important exceptions

Advice about non-securities, such as direct real estate (raw land or buildings), is generally not subject to the Advisers Act — unless the underlying structure still involves securities (e.g., REIT shares, JV interests, fund-of-funds positions, preferred equity, etc.).

“For Compensation”

Compensation includes:

- Advisory fees

- Management fees

- Carried interest

- Commission-like arrangements

- Any economic benefit tied to giving advice

If you are paid to manage or select securities, the Advisers Act likely applies.

Who’s NOT an Investment Adviser? (Statutory Exclusions)

Some categories are explicitly excluded, including:

- Banks

- Lawyers, accountants, engineers, or teachers whose securities advice is incidental to their profession

- Brokers who give only incidental advice and charge no special fee

- General financial publications

- Government securities advisers

- Family offices

These exclusions don’t typically help private fund managers — which is where exemptions come in.

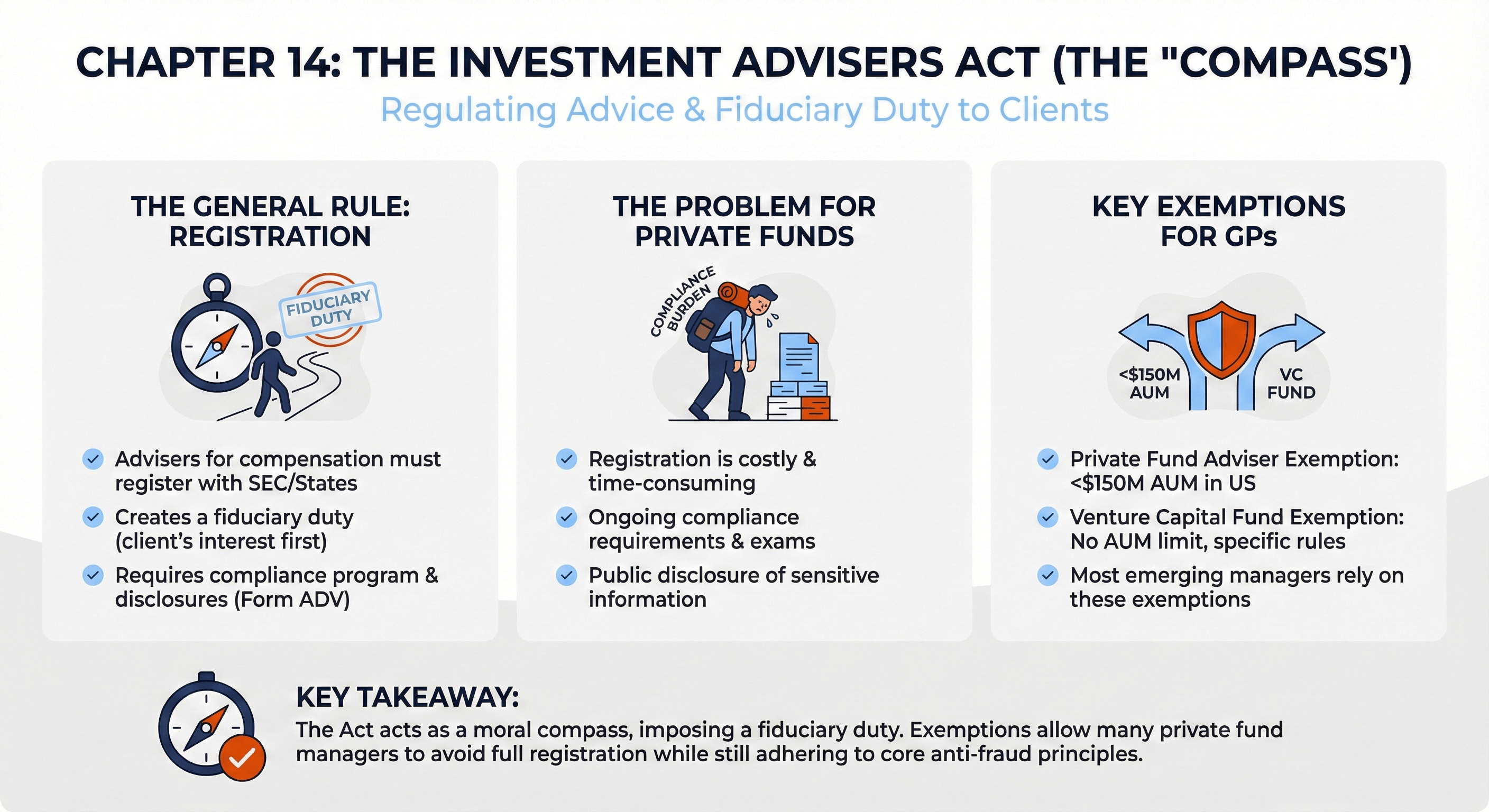

Key Exemptions for Fund Managers

Fund managers typically rely on one of three major exemptions to avoid registering as a Registered Investment Adviser (RIA).

1. Private Fund Exemption — Rule 203(m)-1

This exemption applies to advisers who:

- Manage only private funds, and

- Have less than $150 million in regulatory assets under management (RAUM)

What counts as RAUM?

RAUM includes the gross fair market value of all assets in:

- 3(c)(1) and 3(c)(7) funds

- Fund-of-funds

- Proprietary accounts

- Family accounts

- Accounts managed without compensation

This exemption covers most emerging managers.

2. Venture Capital Exemption — Rule 203(l)-1

This exemption applies to advisers who manage only venture capital funds. VC funds must meet several conditions:

Prong 1: Venture Capital Strategy

The fund must represent that it pursues a VC strategy in its governing documents.

Prong 2: 80/20 Rule

At least 80% of assets must be qualifying investments, meaning:

- Equity securities

- Acquired directly from a qualifying portfolio company

- The company must be:

- Private at the time of investment

- A real operating business

- Not borrowing money to distribute back to the fund

- Not another fund, investment company, or commodity pool

Secondaries are NOT qualifying investments, because they are not purchased directly from the company.

Prong 3: Limited Leverage

Leverage cannot exceed 15% of total contributions and uncalled capital and cannot run longer than 120 days (with narrow exceptions).

Important Warning

You can only use this exemption if you advise venture capital funds and nothing else.

Managing a secondaries fund, credit fund, or hedge-style portfolio can destroy this exemption completely.

3. Foreign Private Adviser Exemption — Rule 202(a)(30)-1

This exemption applies to non-U.S. advisers who:

- Have no U.S. place of business

- Have fewer than 15 U.S. clients and investors

- Have less than $25 million RAUM attributable to U.S. clients/investors

- Do not hold themselves out to the U.S. public as investment advisers

This exemption is narrow but powerful for certain foreign managers.

If No Exemption Applies: You Must Register as an RIA

If you exceed $150 million RAUM — or no exemption applies — you must register with the SEC as a Registered Investment Adviser (RIA).

Registration requires completing Form ADV, a detailed filing split into two major parts.

Form ADV — What’s Required

Part 1

Administrative data:

- Ownership

- Employees

- Regulatory AUM

- Disciplinary history

- Types of clients

Part 2 (the “Brochure”)

Disclosure of:

- Investment strategies

- Fees

- Conflicts of interest

- Risks

- Brokerage practices

- Custody

- Code of ethics

- Disciplinary information

Both parts must be updated annually.

Ongoing Requirements for RIAs

Once registered, RIAs must comply with several regulatory obligations:

1. Custody Rule

Client money and securities must be held with a qualified custodian and are subject to surprise audits.

2. Marketing Rule

Strict standards apply to performance advertising, testimonials, endorsements, and hypothetical returns.

3. Compliance Program

RIAs must:

- Appoint a Chief Compliance Officer (CCO)

- Maintain written policies and procedures

- Conduct an annual review

- Train team members

- Monitor activities continuously

RIA compliance is intensive — and expensive.

Exempt Reporting Advisers (ERAs)

Fund managers who rely on:

- The private fund exemption (under $150M), or

- The venture capital exemption

…are classified as Exempt Reporting Advisers.

ERAs must:

- File Form ADV Part 1A (shorter version)

- Update it annually

- Follow certain recordkeeping rules

- Maintain basic compliance policies

They avoid the burdens of full RIA registration but are not fully unregulated.

About Those (Now Dead) Private Fund Rules…

In 2023, the SEC adopted sweeping new rules regulating private funds, including:

- Mandatory audits

- Side-letter restrictions

- Prohibitions on certain fees

- Detailed quarterly reporting

Then, in 2024, the Fifth Circuit Court of Appeals struck down the entire package. As of now, these rules are not in effect, but the SEC may try to revive or revise them in the future.

What About State Law?

This chapter has focused on federal law.

However, many fund managers — especially those with smaller asset levels — are also subject to state investment adviser laws.

Those rules are covered in the next chapter.

More Fundamentals Chapters

Let's Build Something Together

Please provide some background on yourself, your track record (if applicable), and your goals. We're excited to get started.