How Do You Call Capital from Investors?

Once you’ve officially held your fund’s initial closing, it’s time to get the money! In this chapter, we’ll discuss the process of calling capital from investors. Please note that this chapter has a particular focus on closed-end funds and syndications. Open-end funds—especially hedge funds—often call 100 percent of LP capital and invest it immediately.

Your First Capital Call—Show Me the Money!

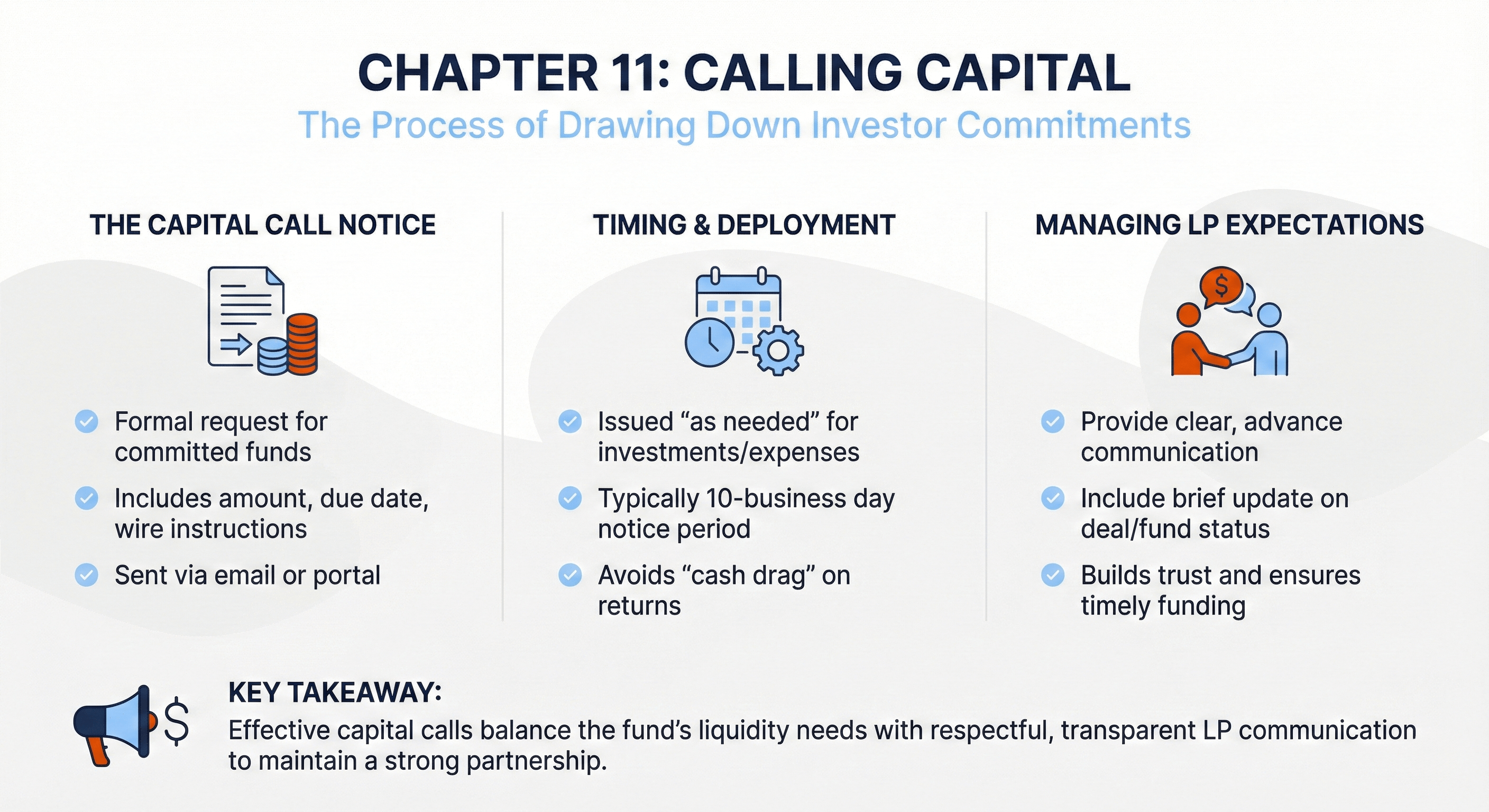

In Chapter 10, we learned how LPs “commit” capital to the fund at the initial closing date. An LP’s capital commitment is the full amount of money the LP has agreed to invest in the fund or syndication. Once the first LPs officially sign the documents and commit, you can issue your first capital call notice to LPs. In this notice, you ask investors to send you money by a certain date. In many fund documents, LPs have ten business days to send the money after the GP calls capital.

An investment fund’s very first capital call often includes money for the following:

• Reimbursing the fund principals for costs incurred to form and raise the fund

• Paying the first quarter’s management fee

• Deploying cash to make the fund’s first investment(s)

• Contributing their pro rata share of warehoused investments (discussed below)

Once you issue the first capital call, you’re off to the races!

Warehoused Investments

In some cases, the GP might identify an asset they want to buy before the fund’s initial closing date. The GP (or their affiliates) might (i) buy this deal themselves and sell it to the fund after the initial closing date, (ii) pre-fund capital contributions into the fund before the official initial closing, or (iii) lend money to the fund before the initial closing date to enable the fund to buy the investment.

In any of the three options above, the fund’s first capital call might include funds to repay the GP (or their affiliates) for the capital contributed (or loaned) to purchase the warehoused investment.

If you’re a GP with a warehoused investment, you should disclose it in your fund documents. LPs should understand the material facts, such as the price you paid and the price the fund will pay (which are often the same price). As these transactions involve conflicts of interest, you must disclose, disclose, disclose!

Why Don’t You Call 100 Percent of the Capital Immediately?

In most multi-asset funds, the GP doesn’t call all the money at once. There are two (related) reasons why you don’t want to call more capital than you actually need.

- IRR Metrics: Internal rate of return (IRR) is a time-based metric. The less time you hold an investor’s dollars, the better your IRR. Therefore, you don’t want to call capital unless you need it for live deals or expenses.

- Preferred Return: The preferred return—like IRR—is calculated based on when the LP’s capital contributions enter the fund. The longer you wait to call capital, the less preferred return accrues.

In practice, the cadence of calling capital varies from fund to fund. On one hand, GPs want IRR to be as high as possible (and the preferred return to be as low as possible). On the other hand, you don’t want to annoy LPs by calling capital every fifteen days just so you can optimize return metrics.

Calling Capital in Single-Asset Syndications

In single-asset syndications, it’s common to call 100 percent of the money at once, especially for venture-capital-style syndications. For some other syndications (such as real estate development), it’s more common to call capital over time.

What Goes in a Capital Call Notice?

Two things absolutely must be in a capital call notice:

- How much money does the LP need to send?

- When is the due date?

Some funds might also require you to specify what the capital will be used for. LPs might request in the LPA (or a side letter) that capital call notices contain a detailed list of uses (e.g., management fees, investments, and other fund expenses).

Capital Calls Are Typically Pro Rata

In most investment funds and syndications, capital calls are pro rata, meaning every investor puts in the same percentage of their capital commitment. For example, at the first capital call, the GP might call 20 percent of each LP’s commitment. There are special circumstances (such as excused investments) where this isn’t the case, but nine times out of ten, capital is called pro rata based on commitments.

Who’s in Charge of Calling Capital?

If the fund has a third-party fund administrator (discussed in Chapter 3), they will handle calculating the capital calls, issuing capital call notices, monitoring incoming wires, and updating the fund’s books and records. If the fund doesn’t have a fund administrator, someone on the GP’s team will be responsible for calling capital. If you have the financial capacity to hire an administrator, it’s often a good idea.

Why Do People on the Internet Sometimes Complain About Capital Calls?

After reading this chapter, you should have a solid understanding of capital calls. But you might be thinking, “Why do people on social media hate capital calls and suggest ‘calling capital’ is a sign of a bad GP?”

Two Types of “Capital Calls”—Mandatory vs. Optional

These disgruntled individuals are usually talking about calls for “additional capital” in syndications. Our internet friends aren’t complaining about the normal fund capital calls we’ve discussed in this chapter. Instead, they’re talking about calls for additional capital above and beyond an LP’s initial commitment.

For example, someone might have a $100,000 commitment to a real estate syndication that has been fully funded. Due to economic conditions or poor execution, the syndication might be in hot water and need additional capital.

Many syndication documents have a mechanism where the GP can issue an “optional” capital call notice to raise extra money. While these capital calls are technically optional, non-funding LPs are typically diluted if they don’t fund the “optional” additional contribution. Some syndication documents have punitive dilution where non-funding LPs really get whacked if they decline to wire additional funds.

So, that’s why some people don’t like capital calls. But now you understand that the calls they are complaining about are not the same as the capital calls in a multi-asset fund that draws down capital over time, which are completely normal.

What Happens If an LP Invests After the Initial Closing Date?

As discussed in Chapter 5, most closed-end funds continue fundraising for twelve to eighteen months after the initial closing date. During that time, the fund typically invests and fundraises simultaneously.

From an accounting perspective, four main things can happen when an LP is admitted during this fundraising window after the fund’s initial closing:

- Equalization of capital contributions (mandatory)

- Penalty interest on equalization amounts (optional)

- Catch-up management fees (optional)

- Interest on management fees (optional)

1. Equalization of Capital Contributions

When a new LP joins a fund, the LP must contribute an amount to the fund such that after the contribution is made, each LP has contributed the same percentage of their capital commitments.

Let’s work through an example. Early Emily joined the fund on the initial closing date with a capital commitment of $100, which she funded immediately. Emily’s funded commitment is $100 and her unfunded commitment is $0.

Late Larry is now joining the fund one year after the initial closing date and has a capital commitment of $100. There are two general ways to handle Larry’s admission. In either case, the result must be that Emily and Larry have funded the same proportion of their commitments.

• Option 1: Larry contributes 100 percent of his capital commitment ($100) and is treated as if he contributed the $100 on the initial closing date.

• Option 2: Larry contributes 50 percent of his capital commitment ($50). The fund then sends that $50 to Emily as a refund. Both have now contributed 50 percent.

After equalization, Emily and Larry are treated as complete equals going forward.

2. Penalty Interest on Equalization Amounts

Most LPAs require late LPs to pay interest to early LPs on these equalization amounts—often prime + 2 percent. This compensates early LPs for taking risk earlier.

The GP usually has the right to waive this interest, and sometimes does, especially for large late-stage LPs. But philosophically, the interest belongs to early LPs, not the GP.

3. Catch-Up Management Fees

Late LPs may need to pay management fees retroactive to the initial closing date. These are typically waivable by the GP.

4. Interest on Management Fees

Some LPAs allow interest on these catch-up fees. Also usually waivable at the GP’s discretion.

Fund Trap #11: Holding Too Many Closings

Most funds try not to hold too many official closings. You must equalize commitments and run all the accounting each time. Better to keep closings limited.

What Happens If an LP Doesn’t Send the Money?

If an LP doesn’t send money after receiving a capital call notice, the fund documents should have a Defaulting Limited Partner section describing the remedies. Common remedies include:

• Default interest

• Suspending distributions

• Forced sale of the LP’s interest

• Lawsuit for specific performance

• Cancellation of the LP’s interest (“the nuclear option”—LPs often negotiate this out)

What Happens in Real Life?

Most GPs try to be reasonable:

• Help the LP sell their interest

• Give an extension

• Excuse the LP

• Modify the capital call

What If an LP Doesn’t Fund Their Very First Capital Call?

Practically speaking: you’re out of luck.

You can theoretically sue, but GPs almost never do. If the LP had the money, they would have funded.

Escrowing LP Funds to Minimize Default Risk

Some GPs require LPs to pre-fund some or all of their commitment into an escrow account. This dramatically reduces default risk, but LPs often dislike it because the money isn’t earning yield.

Sometimes only smaller check-writers must pre-fund into escrow.

More Fundamentals Chapters

Let's Build Something Together

Please provide some background on yourself, your track record (if applicable), and your goals. We're excited to get started.