State Investment Adviser Laws

As mentioned in the last chapter, investment fund managers must deal with state laws if they aren’t RIAs with the SEC.

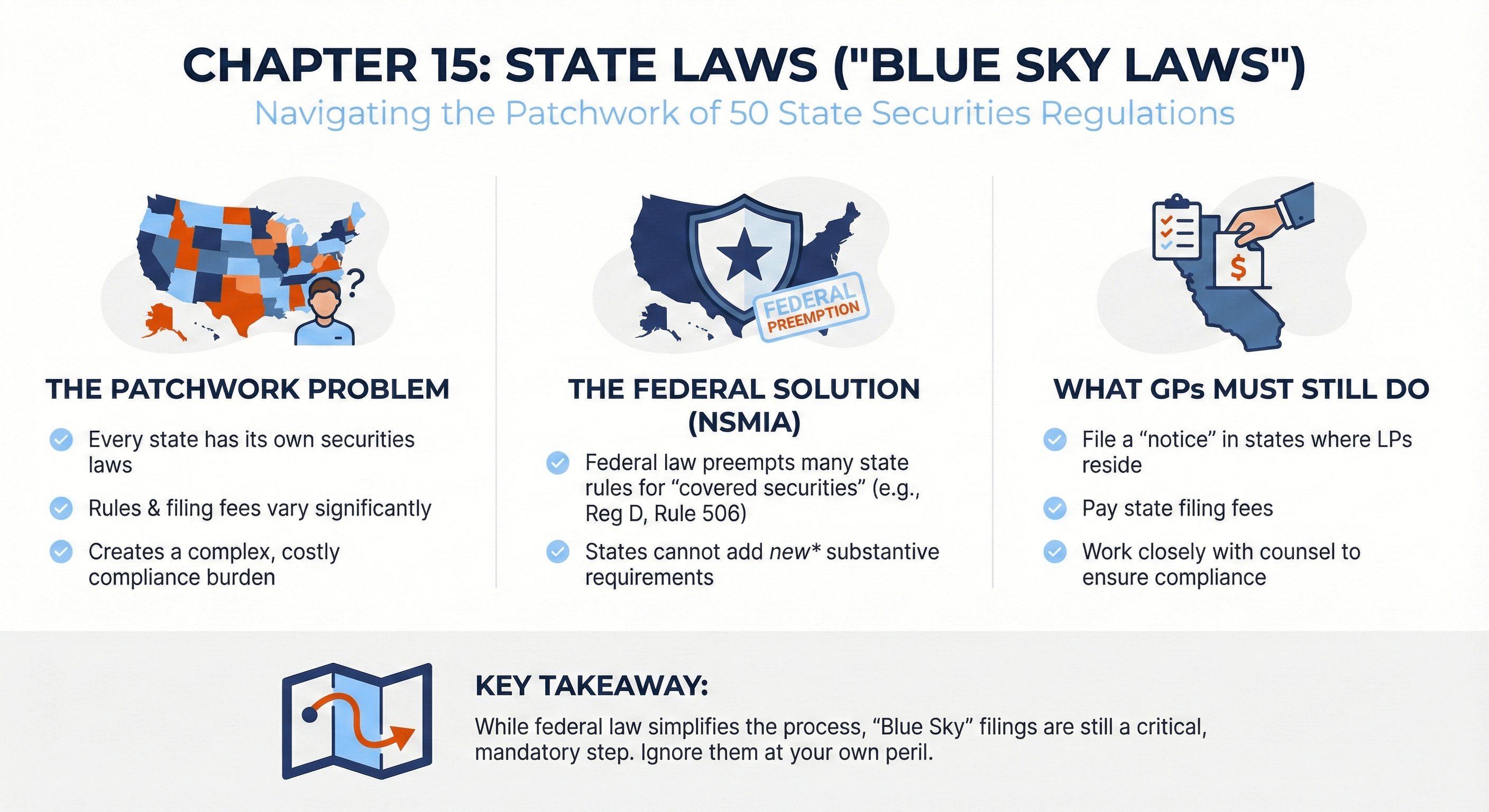

Pursuant to the National Securities Markets Improvement Act of 1996, the federal Investment Advisers Act “preempts” state law once an investment adviser registers with the SEC as an RIA. In other words, once a fund manager is a full-blown RIA, they generally no longer need to deal with state investment adviser laws.

In short: investment fund managers are subject to state investment adviser laws unless and until they become RIAs.

Even fund managers relying on the exemptions from registration we discussed in Chapter 14 are subject to these state laws, including those using the private fund exemption (less than $150 million in assets under management) and the exemption for venture capital fund managers.

If you’re an emerging fund manager (outside certain asset classes like real estate), you likely need to comply with state investment adviser laws. Each state has its own laws. And the states vary wildly on how strict their rules are.

THE NASAA MODEL RULE

Many states have adopted a model rule (or a variation thereof) developed by the North American Securities Administrators Association (NASAA—the same group that helped you transmit Blue Sky filings in Chapter 10). This rule includes registration requirements and exemptions similar to the federal laws we discussed in Chapter 14.

GENERAL REGISTRATION EXEMPTIONS

First, to have a good exemption, there are some generally applicable requirements:

Under the NASAA model rule, private fund advisers can avoid registration with the state if they meet the following requirements:

- neither the private fund adviser nor any of its advisory affiliates are subject to an event that would disqualify an issuer under Rule 506(d)(1) of SEC Regulation D, 17 C.F.R. §230.506(d)(1);

- the private fund adviser files with the state each report and amendment thereto that an exempt reporting adviser is required to file with the Securities and Exchange Commission pursuant to SEC Rule 204-4, 17 C.F.R. § 275.204-4; and

- the private fund adviser pays the fees specified in Section XXX [410 of USA 2002].

In short:

- Bad Actor: The adviser cannot be subject to a “bad actor disqualification”—we discussed this in Chapter 12.

- ERA Filing: The adviser must make an ERA filing with their home state—we discussed ERA filings in Chapter 14.

- Fee: As usual, someone wants a fee.

ADDITIONAL REQUIREMENTS FOR 3(C)(1) FUNDS THAT ARE NOT VENTURE CAPITAL FUNDS

If the adviser has any funds (other than venture capital funds) that rely on 3(c)(1) of the Investment Company Act, they must meet the following additional requirements:

- The private fund adviser shall advise only those 3(c)(1) funds (other than venture capital funds) whose outstanding securities (other than short-term paper) are beneficially owned entirely by persons who, after deducting the value of the primary residence from the person’s net worth, would each meet the definition of a qualified client in SEC Rule 205-3, 17 C.F.R. § 275.205-3, at the time the securities are purchased from the issuer;

- At the time of purchase, the private fund adviser shall disclose the following in writing to each beneficial owner of a 3(c)(1) fund that is not a venture capital fund:

(A) all services, if any, to be provided to individual beneficial owners;

(B) all duties, if any, the investment adviser owes to the beneficial owners; and

(C) any other material information affecting the rights or responsibilities of the beneficial owners. - The private fund adviser shall obtain on an annual basis audited financial statements of each 3(c)(1) fund that is not a venture capital fund, and shall deliver a copy of such audited financial statements to each beneficial owner of the fund.

In short:

- Qualified Clients: The adviser cannot accept investors in any non-venture capital 3(c)(1) fund unless the investors are qualified clients—generally people who have a net worth of $2.2 million or invest at least $1.1 million with the investment adviser.

- Information: The adviser must provide certain information to investors at the time of investment.

- Audit: Each non-venture capital 3(c)(1) fund must have an annual audit and present the results to investors.

If all the adviser’s funds are 3(c)(7) funds, all the adviser’s funds are venture capital funds, or all the adviser’s funds are outside the Investment Company Act’s purview altogether, the adviser would not typically need to comply with these extra rules. Check out Chapter 13 to learn more about 3(c)(1) and 3(c)(7) funds.

⚠ FUND TRAP #15: RAISING A SMALL FUND BEFORE CONSIDERING STATE INVESTMENT ADVISER LAWS

These requirements—especially the “qualified client” and the “audit” provisions—can be quite burdensome for small funds. In fact, small managers seeking to raise a few million dollars may ultimately decline to raise a fund in certain states because the audit requirement is too burdensome or their investor base wouldn’t consist entirely of qualified clients.

The bottom line is that the NASAA model rule isn’t that bad for venture capital managers or managers who don’t need to rely on 3(c)(1). However, for those non-venture capital managers who do need 3(c)(1), the model rule can be a serious roadblock.

More than once, I’ve talked to small private equity fund managers who need to have their financial statements audited to become compliant. They shrivel in despair when they calculate the fee drag an audit will cause on their small fund.

Please, please, please, ask your lawyer about these laws before forming a fund.

SUMMARY OF INVESTMENT ADVISER LAWS IN ALL FIFTY STATES AND WASHINGTON, DC

Now that we understand the NASAA model rule, let’s categorize each of the fifty states into a few buckets. Ultimately, you 100 percent want to work with a lawyer when starting a fund or syndication. This list is just a starting point, and the laws may have changed since this book was published. Alabama and Florida each changed their laws between the first draft of this book and the final version you’re reading today.

If you go to fundamentals.law (our newsletter), you’ll find an article titled “How to Comply with State Investment Advisers Laws,” where we have links to the investment adviser laws for each of the fifty states.

CATEGORY 1: PERMISSIVE

These states are generally quite adviser-friendly. Their rules and requirements for advisers are less burdensome than the NASAA model rule. These states have easy exemptions so long as the total number of “clients” (typically, each fund or syndication is a client) stays below a certain threshold.

- Connecticut: Unlike the NASAA model rule, Connecticut has a “private fund” exemption for managers with less than $150 million in assets under management.

- DC: Unlike the NASAA model rule, Washington, DC, has a “private fund” exemption for managers with less than $150 million in assets under management.

- Florida: Investment managers are exempt from state registration if they have less than six funds/syndications within a twelve-month period. Florida also just added a separate exemption for private fund advisers.

- Georgia: Investment managers are exempt from state registration if they have less than six funds/syndications within a twelve-month period.

- Illinois: Investment managers are exempt from state registration if they have less than five funds/syndications within a twelve-month period.

- Indiana: Investment managers are exempt from state registration if they have less than five funds/syndications within a twelve-month period and a few extra requirements.

- Kansas: Investment managers are exempt from state registration if they have less than fifteen funds/syndications.

- Louisiana: Investment managers are exempt from state registration if they have less than fifteen funds/syndications within a twelve-month period.

- New Jersey: Investment managers are exempt from state registration if they have less than fifteen funds/syndications within a twelve-month period.

- New York: Investment managers are exempt from state registration if they have less than six funds/syndications within a twelve-month period.

- North Carolina: Investment managers are exempt from state registration if they have less than fifteen funds/syndications within a twelve-month period.

- Ohio: Investment managers are exempt from state registration if they have less than fifteen funds/syndications within a twelve-month period.

- Pennsylvania: Investment managers are exempt from state registration if they have less than five funds/syndications within a twelve-month period.

- South Dakota: Exemptions mirror the federal SEC exemptions.

- Tennessee: Investment managers are exempt from state registration if they have less than fifteen funds/syndications within a twelve-month period.

CATEGORY 2: NASAA MODEL RULE

These states adopted the NASAA model rule:

- Alabama

- Colorado

- Iowa

- Massachusetts

- Minnesota

- Nevada

- New Mexico

- Rhode Island

- Virginia

- Wyoming

CATEGORY 3: NASAA MODEL RULE WITH MODIFICATIONS

These states started with the NASAA model rule but tweaked things a bit. You’ll definitely want to check the particulars with your attorney.

- Arizona: Modifications making it more permissive than the NASAA model rule.

- California: Broader venture capital exemption than the NASAA model rule.

- Maine: Only minor modifications.

- Maryland: Only minor modifications.

- Michigan: Audit not required if all investors are qualified clients.

- Missouri: Certain types of accredited investors can be admitted in non-venture capital 3(c)(1) funds even if they are not qualified clients.

- Nebraska: Modifications making it slightly more permissive than the NASAA model rule.

- Oklahoma: Added the $150 million private fund exemption but removed the venture capital exemption.

- South Carolina: Various modifications, some more and some less restrictive.

- Texas: Modifications making it slightly more permissive than the NASAA model rule.

- Vermont: Only minor modifications.

- Wisconsin: In addition to the model rule, Wis. Stat. § 551.403(2)(a)(2m) provides another exemption for advisers whose only clients in Wisconsin are certain categories of accredited investors under federal Regulation D (including entities with total assets in excess of $5 million).

CATEGORY 4: BAD NEWS

These states are more restrictive than the NASAA model rule. In many cases, there are no exemptions whatsoever, meaning an investment adviser must formally register with the state (similar to registering with the SEC as an RIA) no matter what.

- Alaska: No exemptions.

- Arkansas: No exemptions.

- Delaware: Exemption only applies to 3(c)(7) funds.

- Hawaii: No exemptions.

- Idaho: No exemptions.

- Kentucky: Exemption only applies to 3(c)(7) funds.

- Montana: No exemptions.

- New Hampshire: No exemptions.

- North Dakota: No exemptions.

- Utah: Complex provision that is more restrictive than the NASAA model rule.

- Washington: Exemption only applies to 3(c)(7) funds and venture capital funds—not 3(c)(1) funds.

- West Virginia: No exemptions.

CATEGORY 5: OREGON

Oregon exempts “any person who conducts no public advertising or general solicitation in this state and whose only clients in this state are accredited investors.” The question is whether using 506(c) (discussed in Chapter 12) would blow this exemption. I haven’t seen any guidance on this yet. 506(b) appears to be safe. Oregon always needs to do something just a little unusual. Stay weird, my friends.

Next up, the final “real” chapter of this book, where you’ll learn the basics of investment fund tax law

More Fundamentals Chapters

Let's Build Something Together

Please provide some background on yourself, your track record (if applicable), and your goals. We're excited to get started.